Before committing budgets to AI, business leaders want solid proof that the investment will pay off. Investors also keep a close eye on the AI agent market size and funding trends to understand where the real momentum lies. At the same time, product managers look for practical, scalable use cases that genuinely improve productivity and cut operational costs. Developers and researchers focus on performance benchmarks and system efficiency to ensure these solutions actually deliver. In this blog, we share clear statistics on AI agent adoption across industries and compare adoption rates by industry to help you make well-informed decisions.

The market itself is growing steadily, with strong AI agents growth trends expected through 2026. More enterprises are moving from pilot projects to real deployment, and automation is becoming more mature across sectors. Here, we break down the AI agent market forecast and explore the AI agents market size forecast 2026, so you can better understand where the opportunities are heading.

AI agents are no longer just experimental tools. Organizations are actively integrating them into core operations. In AI Agents Statistics 2026: Adoption, Growth & Industry Trends, we cover the latest AI agents statistics, examine real-world adoption rates, and explore how enterprises across major industries are actually using AI agents today.

AI agents began as narrow, rule-based tools for routine tasks like basic chat responses or scripted automation. Their real momentum built after 2023, when large language models allowed systems to plan, adapt, and execute multi-step work with far less oversight. This shift turned early pilots into practical business assets, especially in operations and customer-facing roles.

McKinsey tracks enterprise AI use through yearly executive surveys. In 2024, 78% of organizations used AI in at least one business function. By mid-2025, the share reached 88%. For agents specifically, 62% of companies reported experimenting with AI agents, while 23% had moved to scaling agentic systems in one or more functions.

Gartner forecasts that 40% of enterprise applications will include task-specific AI agents by the end of 2026. This marks a sharp rise from less than 5% in 2025. The research highlights how agentic capabilities are moving quickly from early pilots into production software, especially in workflow-heavy areas.

The Stanford AI Index shows the broader foundation that supported agent growth. Organizational AI adoption climbed from 55% in 2023 to 78% in 2024. That jump in everyday AI use gave companies the data pipelines, skills, and comfort level needed for more autonomous agents to gain traction.

Specialized AI agent market data became more consistent from 2023 onward. Estimates put the global market at roughly USD 3.66 billion in 2023 and USD 5.26 billion in 2024. The steady climb reflects the move from proof-of-concept projects to initial production deployments across sectors.

| Year | Key Development |

|---|---|

| 2023 | 55% of organizations use AI; market ~USD 3.66B |

| 2024 | 78% AI adoption; <1% apps with agentic AI; market USD 5.26B |

| 2025 | 88% AI use; 62% experimenting with agents; 23% scaling |

These AI agents’ statistics reveal a clear pattern: adoption rates stayed modest until the technology matured enough to deliver measurable value. The quick rise from 2023 to 2025 shows how fast organizations recognized the potential once agents could handle real workflows reliably.

Market forecasts for AI agents differ widely because each research firm measures adoption and use cases in its own way. Some reports focus strictly on agentic systems, while others include a broader range of autonomous tools, which naturally shifts the numbers. Looking at each forecast on its own helps you judge which numbers best match your industry, budget, and growth plans.

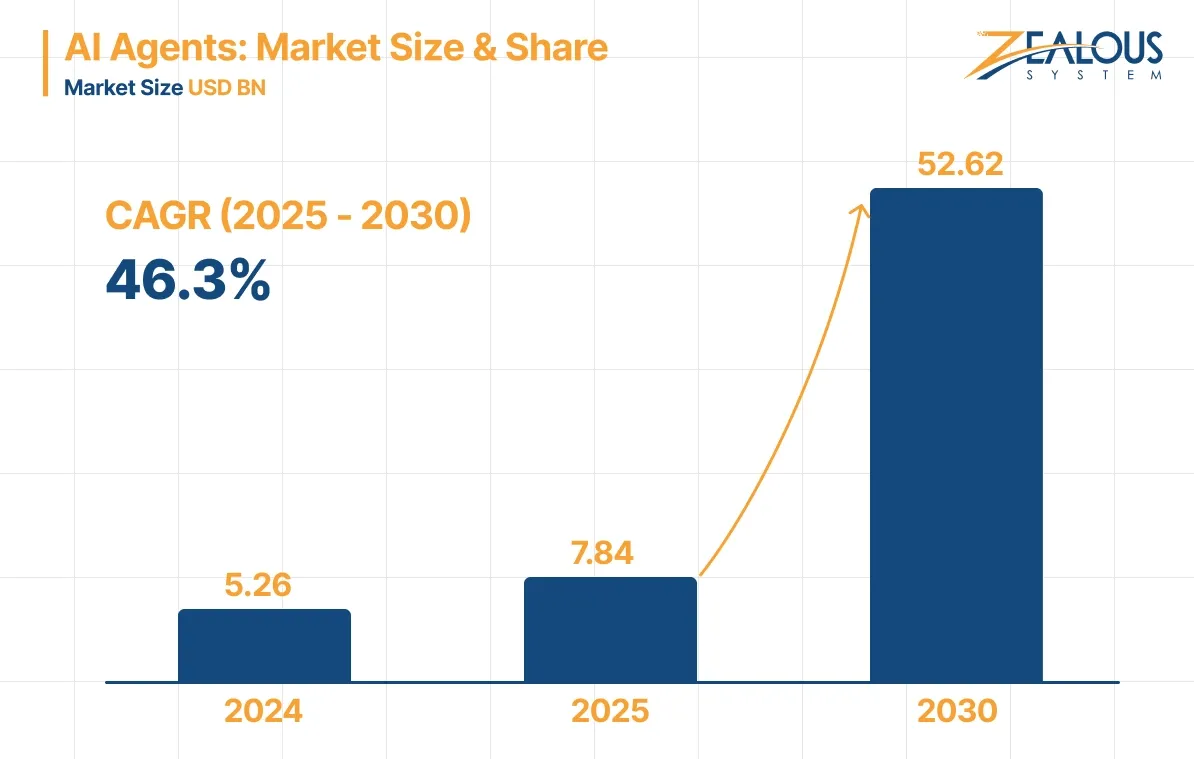

AI agents’ growth trends show the market valued at USD 5.26 billion in 2024, set to reach USD 52.63 billion by 2030. This reflects a 46.3% CAGR, driven by automation demands in enterprises. Such AI agent statistics highlight opportunities in ready-to-deploy solutions for quick integration.

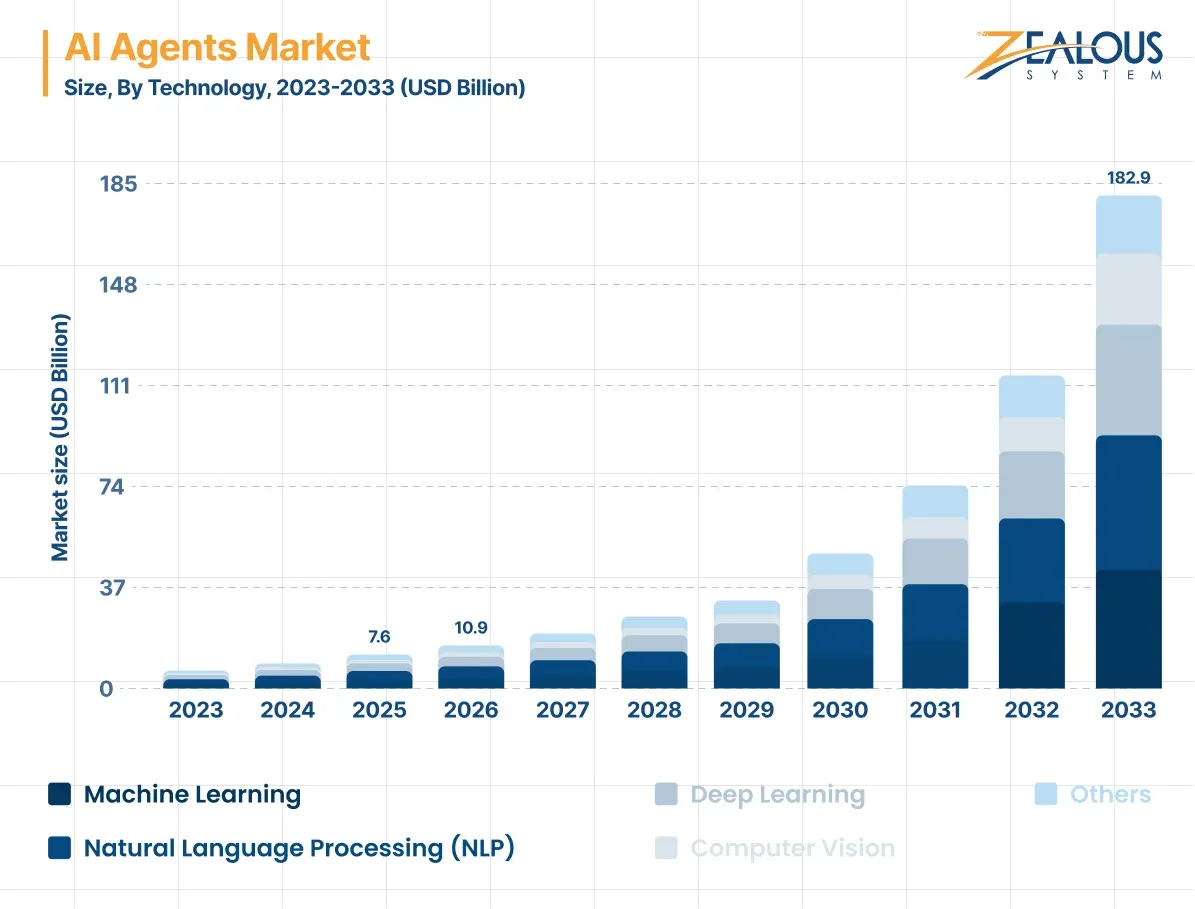

According to this analysis, the AI agent market size starts at USD 7.63 billion in 2025, growing to USD 10.91 billion in 2026 and USD 182.97 billion by 2033. The 49.6% CAGR accounts for advances in multi-agent systems and applications in healthcare. This AI agent market forecast emphasizes North America’s lead in adoption.

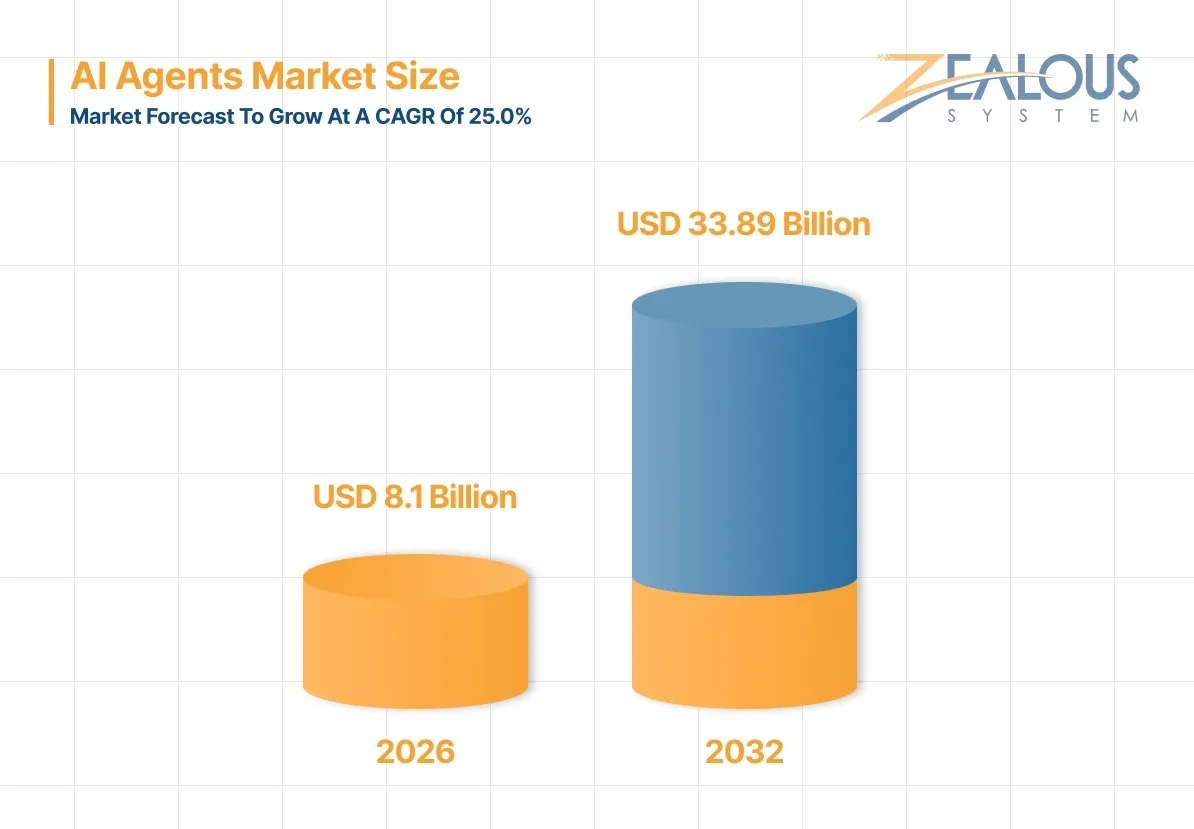

This report pegs the market at USD 7.12 billion for 2025, rising to USD 8.81 billion in 2026 and USD 33.89 billion by 2032. With a 24.95% CAGR, it focuses on regulatory and infrastructure factors across regions. These numbers underscore AI agent adoption rates in sectors like banking and manufacturing.

All three reports agree on one clear direction: rapid expansion is underway, with North America leading and multi-agent systems gaining share.

| Source | 2026 Market Size (USD Bn) | Endpoint Projection | CAGR |

|---|---|---|---|

| MarketsAndMarkets | 11.5 | 52.62 by 2030 | 46.3% (2025-30) |

| Grand View Research | 10.91 | 182.97 by 2033 | 49.6% (2026-33) |

| ResearchAndMarkets | 8.81 | 33.89 by 2032 | 24.95% (2026-32) |

The wide range of CAGRs (25% to nearly 50%) reflects different assumptions about how quickly organizations will move from pilots to full production use. For business leaders and investors, this spread signals both opportunity and the need for careful vendor evaluation. The consistent message across all sources is that AI agent adoption rates are accelerating right now, making 2026 a pivotal year for securing a competitive advantage through automation.

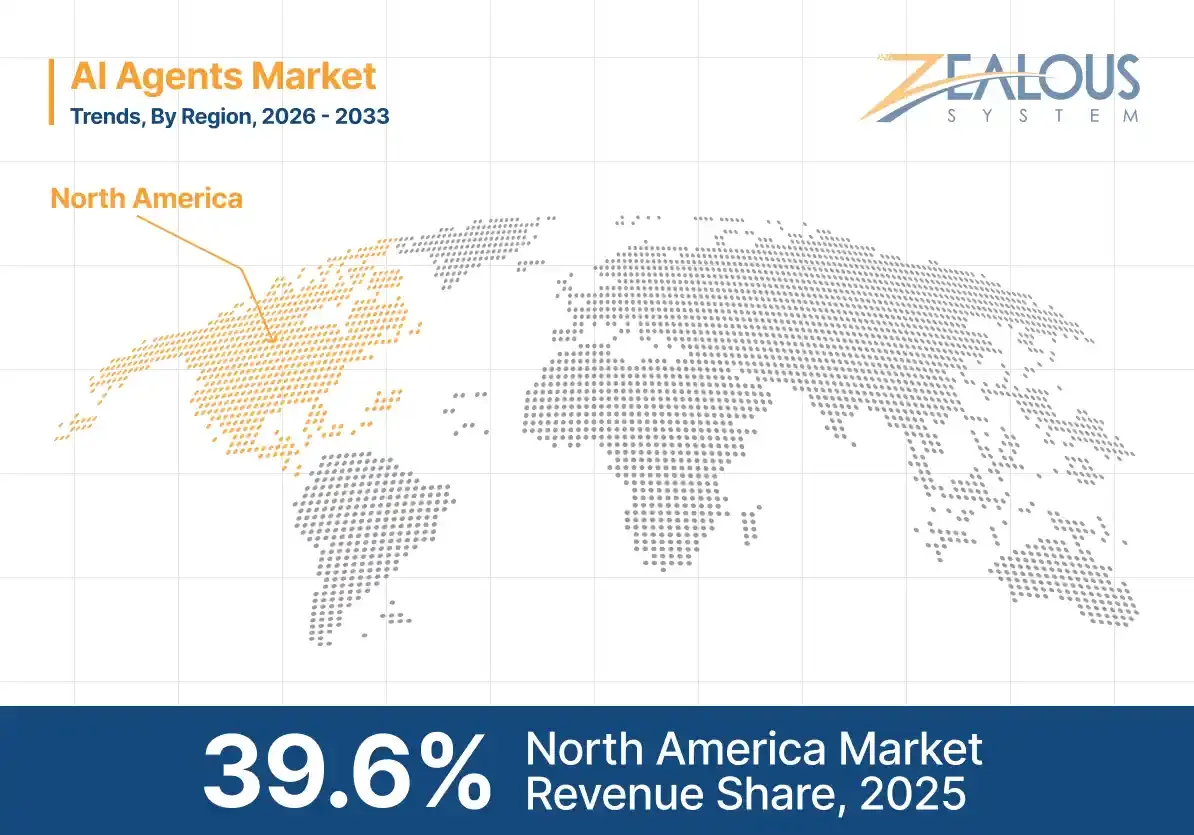

Adoption levels differ sharply by region, largely based on how advanced local infrastructure is and how aggressively companies are investing in AI right now. North America leads in current share, while Asia Pacific shows the strongest momentum for near-term expansion. For investors and operators, these patterns make it easier to spot where growth is accelerating and where adoption may lag.

North America holds the dominant position, accounting for approximately 39.6% of global revenue share in 2025 (with projections maintaining leadership through 2033). The region’s advantage comes from advanced technological infrastructure, a high concentration of leading AI companies, substantial R&D investments, and early integration across sectors such as healthcare, finance, defense, and retail. The United States drives the majority of this share through enterprise-scale deployments, innovation ecosystems, and supportive venture funding.

Asia Pacific is the fastest-growing region, with CAGRs frequently exceeding 50% (e.g., 53.2% from 2026 to 2033). Rapid digital transformation, expanding manufacturing and e-commerce sectors, rising internet penetration, supportive government policies, and increasing disposable income fuel this acceleration. Key contributors include China, Japan, India, and South Korea, where large-scale industrial applications and consumer-facing AI drive demand.

Europe benefits from strong regulatory frameworks (such as the EU AI Act) and a growing emphasis on responsible, trustworthy AI deployment. Growth occurs in manufacturing, healthcare, energy, and public sector applications, though the region trails North America in current market share. Focusing on ethical AI, data privacy, and cross-border collaboration shapes adoption patterns here.

Latin America and the Middle East & Africa represent smaller but emerging markets. Their growth comes mainly from expanding digital systems, better connectivity, and rising demand from companies looking to automate everyday operations. Adoption remains at earlier stages compared to North America, Asia Pacific, and Europe.

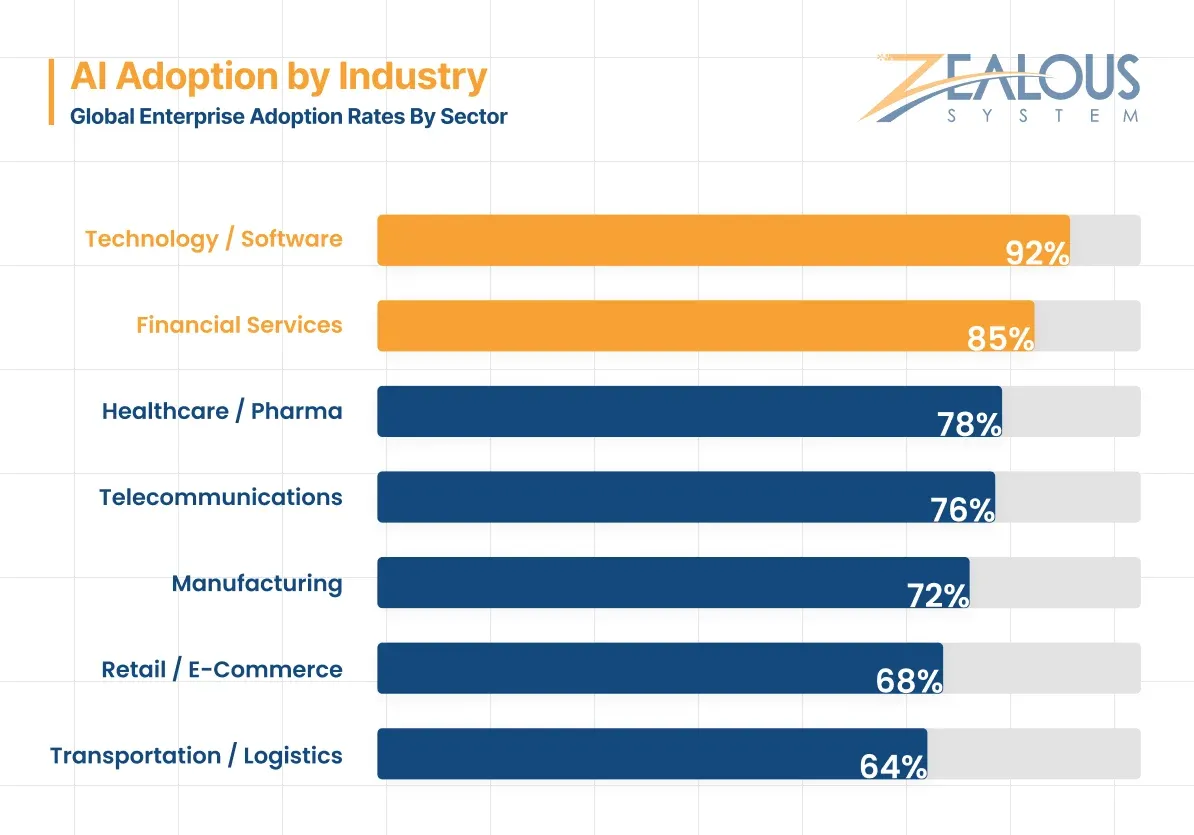

AI agent adoption rates by industry show clear differences in pace and focus as of early 2026. Some sectors push ahead with scaled deployments, while others concentrate on high-value pilots that deliver quick wins. These statistics on AI agent adoption across industries give tech leaders and decision-makers a practical map of where real momentum exists right now.

This group leads in AI agent deployment. Agents support IT service desks, automated research, and complex workflow coordination. McKinsey data shows the highest agent usage here compared to other industries, with many organizations reporting production-level integration.

Healthcare ranks second in agent adoption. Agents reduce administrative tasks, assist in clinical workflows, and enable ongoing patient monitoring. Organizations in this sector often build comprehensive AI strategies that incorporate agents for end-to-end support, improving efficiency while preserving accuracy.

Financial services apply agents for fraud detection, compliance monitoring, and real-time risk assessment. Adoption remains strong in regulated settings, where agents handle repetitive analysis and allow faster decisions on high-volume transactions.

Retailers and eCommerce platforms use agents for personalized recommendations, inventory optimization, and order processing. Steady uptake focuses on continuous operations that boost conversion rates and supply chain agility.

Manufacturing deploys agents for predictive maintenance, quality control, and supply chain coordination. Agents run continuously to cut downtime and adjust production dynamically, delivering direct gains in equipment reliability and reduced waste.

Customer service shows some of the quickest gains. Agents manage routine queries, escalate complex cases, and ensure consistent multi-channel support. Projections indicate broad adoption by late 2026, with many teams already reporting faster resolutions and higher productivity.

Together, these numbers show that tech companies and healthcare providers are moving fastest, with other industries following close behind in targeted areas. Adoption remains uneven overall, but the business value in high-volume or repetitive tasks drives faster integration where it fits best.

Most companies bring in AI agents to save time, cut operational costs, automate complex workflows, and stay ahead of competitors already using the technology. Data from major surveys shows strong momentum on the motivation side, while integration, governance, and risk issues remain the biggest roadblocks.

These numbered AI agents statistics highlight the current reality in 2026: strong productivity and budget signals are pushing adoption forward, while legacy integration, governance gaps, and ROI uncertainty continue to slow many organizations from moving beyond pilots.

AI agents in 2026 deliver tangible performance improvements across productivity, efficiency, and customer interactions. In real deployments, teams complete tasks faster, resolve issues sooner, and spend far less on day-to-day operations. For leaders evaluating budgets and ROI, these benchmarks make the business case far clearer.

Employees using AI agents achieve noticeable time savings and output increases. Contact centers with autonomous agents reduce cost-per-contact by 20% to 40% through higher Tier-1 resolution rates. IT teams deploying self-healing agents cut mean time to resolution by 30–50%. In banking, loan origination processes approve applications 40% faster while reducing fraud by 35%.

Broader studies indicate most enterprises see 10–15% average productivity gains from AI, though end-to-end workflow deployments can yield up to 210% ROI with quick payback periods. High performers report stronger results, with agents handling repetitive tasks to free humans for strategic work.

| Metric | Typical Gain | Notes / Context |

|---|---|---|

| Productivity | 10–15% average; up to higher in workflows | Broad enterprise studies |

| Contact Center Costs | 20–40% reduction | Via higher first-contact resolution |

| IT Resolution Time (MTTR) | 30–50% faster | Self-healing agents |

| ROI in End-to-End Deployments | Up to 210% | Quick payback in targeted use cases |

AI agents support creative processes by accelerating ideation and iteration. Marketing teams using agents for campaign development achieve 73% faster timelines and 68% shorter content creation cycles. Analytics agents improve sales forecast accuracy by 38%, allowing teams to focus on strategy over manual data handling. Overall, agents shift focus from routine execution to higher-level innovation and problem-solving.

AI agents handle increasing shares of interactions autonomously. Projections show customer support approaching 80% autonomous resolution for routine queries, cutting operational workflow costs by 40–60%. Consumers respond positively in many cases, with 70% willing to let agents book flights independently and 65% trusting them for hotel selections.

Positive experiences are tied to brand perception. Fast, consistent AI-driven interactions contribute to stronger views, though balanced human oversight remains key for complex needs.

By the end of 2026, 40% of enterprise applications are expected to embed task-specific AI agents, up from less than 5% in 2025. Enterprise adoption of autonomous agents hovers around 37% in some estimates, with scaling still challenging for many organizations.

These AI agent performance and impact statistics demonstrate clear value in targeted deployments. Productivity lifts of 10–50% in specific functions, combined with efficiency gains and customer handling improvements, position agents as practical tools for competitive advantage in 2026.

By the end of 2026 and into the following years, AI agents are set to shift from experimental tools to core components of enterprise operations. Analysts expect AI agents to be built directly into everyday software, work together in coordinated systems, and take over large parts of routine workflows. These predictions help tech professionals, leaders, and investors gauge the realistic pace of change ahead.

Task-specific AI agents will see rapid uptake in applications. Gartner forecasts that 40% of enterprise applications will feature these agents by the end of 2026, rising from less than 5% in 2025. This marks a key step toward agents handling proactive, workflow-oriented tasks rather than simple assistance.

Single agents will evolve into coordinated teams. Predictions highlight multi-agent orchestration as a breakthrough in 2026, with dozens or hundreds of specialized agents collaborating on complex processes like supply chain optimization or R&D pipelines. Such systems enable longer-running, autonomous operations with minimal human intervention beyond strategic oversight.

AI agents will act more like digital coworkers and teammates. In 2026, expect agents to manage entire workflows, boost productivity by automating routine and complex tasks, and enable concierge-style customer service through personalized, proactive interactions. Companies will increasingly focus on training employees to collaborate effectively with these systems, shifting roles toward orchestration and higher-value work.

The agentic AI landscape is shaped by leading developers and platforms:

While momentum builds, challenges persist. Gartner predicts over 40% of agentic AI projects could be canceled by the end of 2027 due to rising costs, unclear value, or weak risk controls—implying some slowdowns starting in 2026. Strong governance will prove essential for scaling beyond pilots, especially as agents gain autonomy in decision-making.

Looking beyond 2026, projections include 90% of B2B buying intermediated by AI agents by 2028 (driving over $15 trillion in spend through agent exchanges) and 15% of day-to-day work decisions made autonomously by the same timeframe. These timelines underscore how agents could reshape procurement, productivity tools, and daily operations in the coming years.

These future predictions for AI agents in 2026 emphasize acceleration in practical deployment and collaboration, balanced against the need for careful risk management. Organizations that address integration and governance early stand to capture the most substantial gains in efficiency and competitive positioning.

Real-world AI agent deployments in 2026 show clear results in efficiency, customer engagement, and operational scale. These two examples from major enterprises highlight how agents handle proactive, multi-step tasks in banking and retail, providing practical benchmarks for evaluation.

Bank of America’s Erica, launched in 2018, is an AI-powered virtual assistant built into the mobile banking app. By 2025, it had handled over 3 billion client interactions for nearly 50 million users, averaging more than 58 million interactions per month.

Erica manages routine tasks like balance checks, fund transfers, bill payments, spending tracking, and personalized financial advice, significantly increasing self-service rates while reducing demand on human support teams in a highly regulated environment.

Amazon’s Rufus is a conversational AI shopping assistant integrated into the app that helps customers find products through natural language questions and offers personalized recommendations. Usage of Rufus grew rapidly (127% during peak shopping periods in late 2025), improving discovery and decision speed for shoppers.

In parallel, Amazon’s supply chain agents optimize inventory placement, warehouse picking, packing, and delivery routing by coordinating complex, multi-step logistics tasks, which reduces delays, lowers costs, and improves overall operational reliability.

In 2026, AI agents have shifted from experiments to essential business tools. Companies now partner with an experienced AI development company to move faster from pilot projects to real deployment. Adoption rates continue to rise because organizations see measurable productivity gains, stronger workflow efficiency, and meaningful cost savings across customer service, finance, and retail. Forecasts show rapid market growth, deeper integration into enterprise software, and multi-agent systems emerging as the next major step forward.

The data clearly shows that success depends on focused, high-ROI use cases, strong governance frameworks, and thoughtful integration planning. Many enterprises invest in specialized AI software development services to ensure seamless deployment, scalability, and compliance from day one. Legacy compatibility and risk management still present challenges, but companies that address them early build sustainable competitive advantages.

The biggest opportunity now lies in strategic deployment. Businesses that treat AI agents as core digital assets rather than optional add-ons unlock stronger efficiency, faster innovation cycles, and improved customer outcomes. With the right technology partner and long-term roadmap, AI agents can deliver measurable impact across the entire organization.

If you’re ready to build or integrate custom AI agents for your workflows, working with a proven AI agent development company can help you move faster and avoid common setbacks.

These FAQs address the most common questions from tech professionals, business leaders, and decision-makers reviewing AI agents’ statistics and trends in 2026.

1. What is the current AI agent market size in 2026?

The AI agent market size in 2026 ranges from approximately USD 8.8 billion to USD 10.9 billion, depending on the research firm and scope (e.g., ResearchAndMarkets: ~8.81B, Grand View Research: ~10.91B). Most credible forecasts place it in the USD 8–11 billion range.

2. How fast is the AI agent market growing?

CAGR estimates vary by source: 24.95% (ResearchAndMarkets to 2032), 44.8–46.3% (MarketsAndMarkets to 2030), and up to 49.6% (Grand View Research to 2033). The consensus shows very strong double-digit annual growth through the late 2020s.

3. Which industries are adopting AI agents the fastest in 2026?

Technology/media/telecommunications and healthcare lead in deployment scale and maturity. Financial services, retail/e-commerce, manufacturing, and customer service follow closely, with the highest reported agent usage in workflow-heavy and customer-facing functions.

4. What are the main reasons companies adopt AI agents right now?

The top drivers are productivity gains (66% of users report measurable improvements), cost reduction in repetitive tasks, and competitive pressure. 88% of senior executives plan to increase AI budgets specifically because of agentic capabilities.

5. What are the biggest challenges stopping wider AI agent adoption?

Legacy system integration (cited by ~60% of AI leaders), weak governance (only 21% have mature models), unclear ROI, high project costs, and data quality/access issues remain the primary barriers. Over 40% of agentic projects are at risk of cancellation by 2027.

6. What will AI agents look like in enterprises by the end of 2026 and beyond?

By end-2026, ~40% of enterprise applications are expected to include task-specific AI agents (up from <5% in 2025). Multi-agent systems that collaborate autonomously on complex workflows will become more common, with agents increasingly acting as digital teammates for entire processes.

Our team is always eager to know what you are looking for. Drop them a Hi!

Pranjal Mehta is the Managing Director of Zealous System, a leading software solutions provider. Having 10+ years of experience and clientele across the globe, he is always curious to stay ahead in the market by inculcating latest technologies and trends in Zealous.

Comments